CashLine x Visa | Business Solution Concept Note

Prepared April 2026

Proposed For Visa

Visa-Enabled Digital Subsidy and Trade Payment Solution for Libya

A structured market-entry model that formalizes subsidy-linked value flows, captures downstream FX activity inside a controlled digital workflow, and positions Visa where it can deliver the strongest commercial and strategic impact.

Executive position

This concept does not attempt to overwrite Libya's real market behavior. Instead, it digitizes the existing cycle through CashLine as the domestic orchestration and control layer, while reconnecting Visa to the ecosystem through beneficiary access credentials and formal outbound merchant-payment rails.

Contents And Positioning

Document Guide

The note is structured to move from market context, to solution design, to commercial fit for Visa.

Problem

Design

Stakeholders

Workflow

Value

Roadmap

The recommended Visa story is deliberately focused. Visa is not asked to own the entire domestic subsidy process. The model instead places Visa in two natural value zones: beneficiary access and formal outbound payment rails. That positioning makes the solution more realistic for regulators, local institutions, and market adoption.

Strategic thesis

Libya's subsidy-linked value flow has not disappeared. It has simply migrated across less visible channels. The strongest opportunity is therefore not to resist the market cycle, but to structure it, digitize it, and redirect commercially meaningful portions back to formal payment infrastructure.

Design standard

This rewritten package is designed for executive review: concise hierarchy, monochrome print fidelity, clean vector diagrams, and language suitable for strategic solution discussion with Visa and regulated partners.

Sections 1 And 2

Executive Summary And Market Context

Low visibility

Fragmented rails

Weak formal capture

1. Executive summary

The current Libya subsidy-disbursement model has reduced the role of formal card-based payment infrastructure without eliminating the downstream foreign-exchange market. Value still moves from formal allocation into resale, unofficial transfer behavior, and trade-payment activity that sits outside a fully visible digital environment.

CashLine proposes a pragmatic Visa-enabled re-entry model. Rather than attempting to redesign the market around an idealized operating pattern, the solution formalizes the existing cycle through CashLine as the domestic orchestration and system-of-record layer. Visa is positioned where it fits naturally and credibly: issuing-linked beneficiary access and formal outbound payment rails.

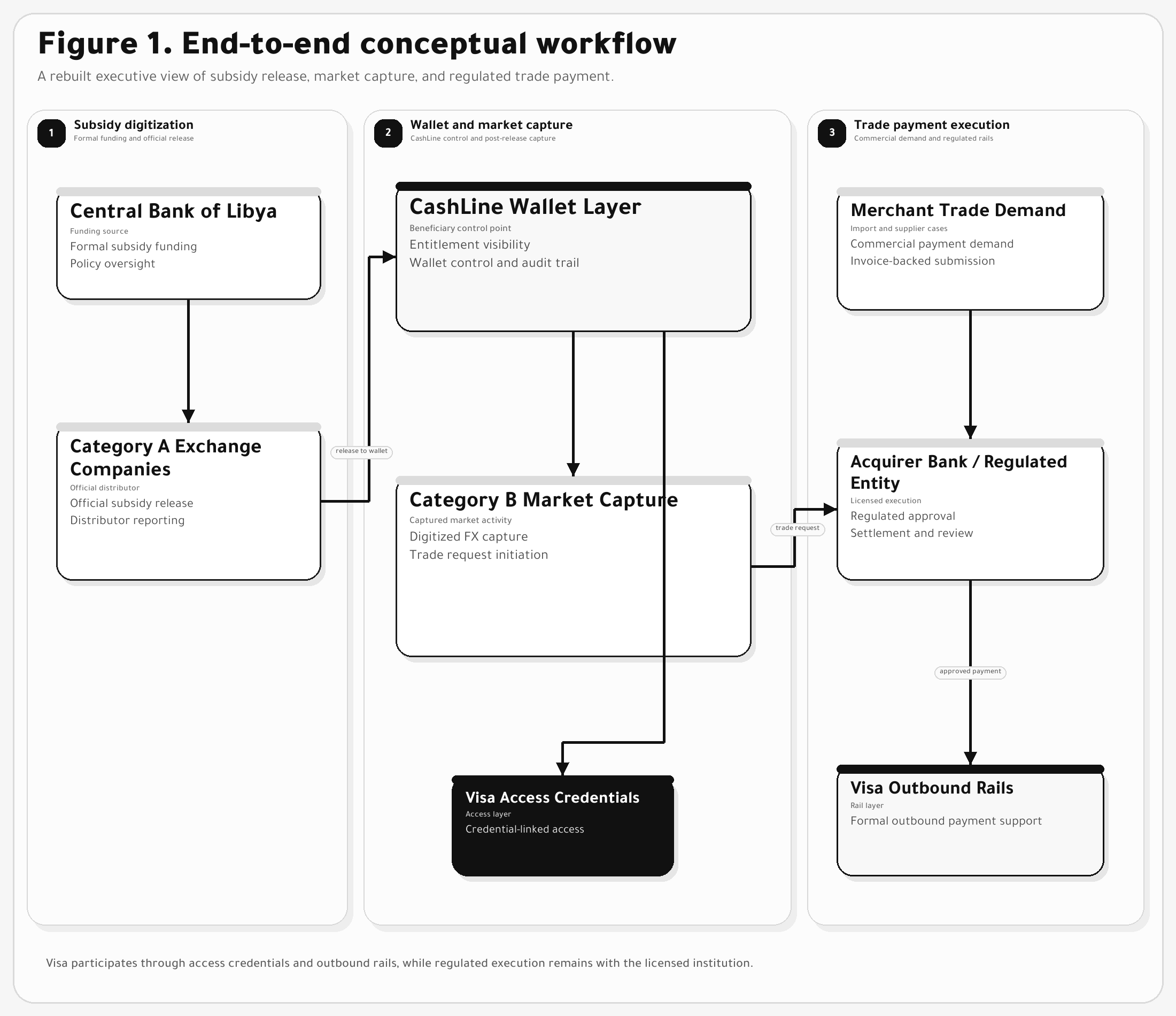

In the target model, the Central Bank of Libya continues to fund Category A exchange companies through the formal channel; beneficiaries draw full or partial value into CashLine wallets with optional Visa-linked access; post-release FX activity involving Category B is digitized rather than ignored; and merchant trade payments move through a regulated execution institution using Visa-connected outbound rails.

2.1 Market condition

Libya's earlier subsidy models relied more directly on bank-issued cards for household access. Over time, exchange-rate volatility, liquidity behavior, and uncertainty in the wider market reduced the effectiveness of that channel. The market adapted, but the new structure shifted value away from transparent digital capture.

2.2 Business problem

The real challenge is deeper than subsidy distribution. The current model allows formally allocated value to migrate into informal FX capture and unofficial cross-border settlement patterns. That reduces regulatory transparency, weakens digital-payment participation, and limits Visa's relevance inside an important transaction ecosystem.

Any workable solution must respect how the market actually behaves. Householders, Category A exchange companies, Category B participants, merchants, and licensed financial institutions are all responding to strong incentives. The model succeeds by digitizing those realities, not by pretending they can be removed by policy language alone.

Sections 3 And 4

Design Logic And Stakeholder Architecture

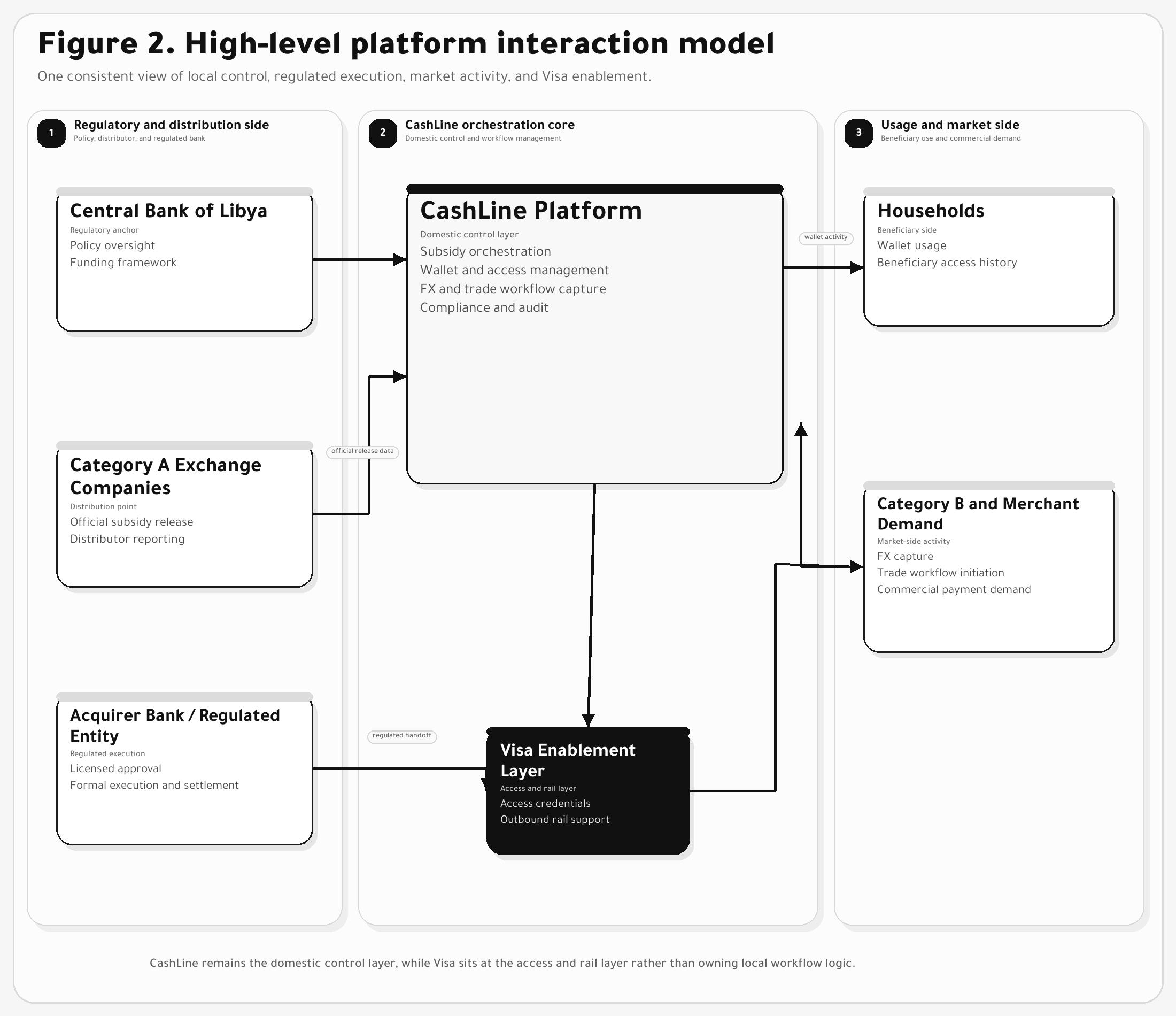

CashLine control

Visa access

Regulated execution

3. Design logic of the proposed solution

- Preserve real economic behavior instead of forcing an artificial local operating model.

- Use CashLine as the orchestration, compliance, and system-of-record platform for all domestic workflow events.

- Keep Category A exchange companies as the official subsidy release point already accepted by the market.

- Digitize Category B as a visible participant in post-release FX activity and merchant trade-payment initiation.

- Position Visa at the beneficiary-access and outbound-rail layers where it creates the strongest strategic value.

- Maintain formal payment execution with the Acquirer Bank or other regulated entity.

| Design question | Recommended answer | Business rationale |

|---|---|---|

| Who owns domestic workflow control? | CashLine | Creates one auditable platform for allocation, wallet activity, FX capture, trade workflow, reporting, and controls. |

| Who releases subsidy value? | Category A exchange companies | Preserves the role already legitimized in the market and avoids unnecessary structural disruption. |

| How does Visa re-enter the ecosystem? | Wallet-linked access credentials and outbound payment rails | Allows Visa to participate in high-value touchpoints without taking ownership of local subsidy administration. |

| What happens to Category B activity? | It is digitized and monitored rather than excluded | Converts an existing market leak into a controlled and commercially useful workflow. |

| Who performs regulated outbound execution? | Acquirer Bank or regulated financial entity | Keeps settlement and compliance responsibilities with a licensed institution. |

| Stakeholder | Primary role | Why included | Value gained |

|---|---|---|---|

| Central Bank of Libya | Policy authority and oversight | Owns subsidy framework and requires stronger digital visibility | Better transparency, reporting discipline, and auditability |

| Category A exchange companies | Official subsidy distributor | Receive formal funding and release subsidy value to beneficiaries | Operational digitization and clearer reporting |

| Householders | Subsidy beneficiaries | Receive and use subsidy-linked value | Faster access, better visibility, and optional credential-linked usage |

| Category B participants | Digitized FX and trade actors | Buy post-release USD and initiate merchant-payment workflow | Operational legitimacy, workflow efficiency, and formal rails |

| Merchants | Trade-payment demand originators | Supply invoices and supporting documents for commercial payments | Structured submission, status visibility, and more reliable processing |

| Acquirer Bank / regulated entity | Licensed execution institution | Owns approval, origination, and settlement of formal outbound payments | Formal payment volume and fee generation |

| Visa | Access credential and rail partner | Supports beneficiary access and regulated outbound merchant-payment rails | Strategic re-entry into the subsidy-linked ecosystem |

Sections 5 And 6

Conceptual Workflow And Platform Model

Subsidy digitization

FX capture

Trade payment

The target workflow contains three linked business legs: subsidy digitization, market resale capture, and merchant trade payment.

The interaction model centers CashLine as the domestic control layer while keeping regulated execution and Visa participation clearly separated.

Sections 7 And 8

Value Proposition For Visa And The Wider Ecosystem

Access

Rails

Strategic relevance

| Value area | What the proposed solution delivers to Visa |

|---|---|

| Re-entry model | A credible route back into the Libya subsidy-linked ecosystem without re-creating the old card-only model. |

| Issuing opportunity | A beneficiary-access model tied to wallet usage and credential activation rather than only bank-card distribution. |

| Cross-border payment relevance | A formal merchant-payment path executed by a regulated institution using Visa-connected outbound rails. |

| Strategic ecosystem position | Participation in both the consumer-access layer and the commercial outbound-payment layer. |

| Partner alignment | A clear narrative that can be discussed coherently with regulators, exchange companies, and licensed banking counterparts. |

The model does not ask Visa to solve every domestic operational issue. It creates a concentrated role at the access and rail layers, which is strategically cleaner, more scalable, and more realistic for adoption. Because Category A, Category B, and the regulated institution remain in their natural operating positions, Visa can engage from a position of relevance without becoming the local process owner.

| Stakeholder group | What changes under the proposed model | Why it matters |

|---|---|---|

| Central Bank of Libya | Receives digital visibility across allocations, withdrawals, FX capture, and trade-payment events. | Supports stronger oversight, reporting, and control. |

| Category A exchange companies | Move from fragmented subsidy handling into a structured digital operating workflow. | Improves operational efficiency and settlement clarity. |

| Householders | Gain wallet-based access, transaction history, and optional Visa-linked usage. | Improves usability without removing beneficiary flexibility. |

| Category B participants | Become digitally captured actors inside FX and trade-payment activity. | Reduces leakage and converts market reality into a visible workflow. |

| Merchants | Receive a cleaner route for documentation, submission, and payment-case tracking. | Improves reliability and commercial confidence. |

| Acquirer Bank / regulated entity | Own formal approval and execution of outbound payments. | Keeps settlement aligned with regulatory expectations and fee activity. |

Sections 9 And 10

Scope, Roadmap, And Closing Position

Scope

Pilot

Alignment

| Component | Conceptual scope |

|---|---|

| Subsidy orchestration | Funding-file intake, entitlement logic, Category A allocation visibility, release controls, and exception handling. |

| Wallet and access layer | Multi-currency wallet, balance visibility, transaction history, and Visa-linked beneficiary access credentials. |

| Category A operations | Release workflow, reporting, cashout handling, and distributor controls. |

| Category B market capture | FX purchase capture, trade-request intake, documentation, and post-release liquidity workflow. |

| Merchant trade-payment workflow | Invoice capture, supplier details, purpose-of-payment data, case progression, and status tracking. |

| Compliance and controls | KYC and KYB checks, source-of-funds logic, screening, alerts, audit trails, and reporting. |

| Formal payment execution | Acquirer Bank or regulated entity execution supported by Visa-connected outbound payment rails. |

The solution does not seek to erase the current market cycle. It turns that cycle into a visible, controlled, and fee-generating ecosystem, with Visa participating as a strategic partner in household access and formal outbound payment execution.

10. Recommended next steps

The strongest route back into this ecosystem is not to deny the market's current behavior, but to formalize it, digitize it, and connect it to a structure where Visa can create visible value.